|

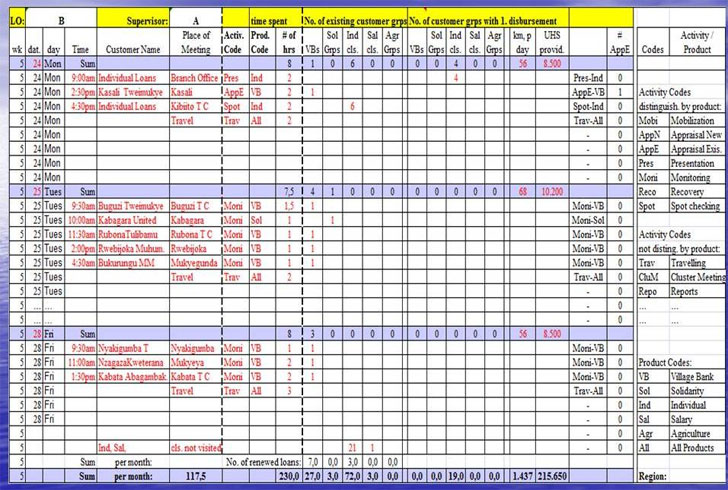

Asking loan

officers and their supervisors to report their activities on a regular

basis in an electronic format the foundation for improving the strategic

planning model developed earlier for the institution as well as to build a performance model for loan officers

was set:

Incorporating the work plans into the strategic planning model, more precise estimates of time spent by loan officers per product type per branch could be derived. On the other hand the parameters driving all costs and income items in this planning model could in turn be used to calculate each LO’s individual net margins, i.e. income minus costs, with respect to their outstanding portfolios in each loan product served. In order to achieve the latter task those costs that aren't directly related to the activities of the loan officers and their supervisors are also broken down to a single loan in an automated fashion.

The resulting performance model displays for each loan officer all key influencing parameters per product type such as the average outstanding loan amount per loan and total together with the respective associated margins, monthly loan loss rates, etc. This allows supervisors to analyse conveniently in which way the performance could be improved and to advise their respective loan officers accordingly.

|